You don’t stick with a bank because the logo feels comforting or the branch is on your street. You stick because the bank becomes the default place where your financial routine works. Salary comes in. The same bills go out. The same services are renewed. After a month, your account turns into a quiet system that runs your life in the background.

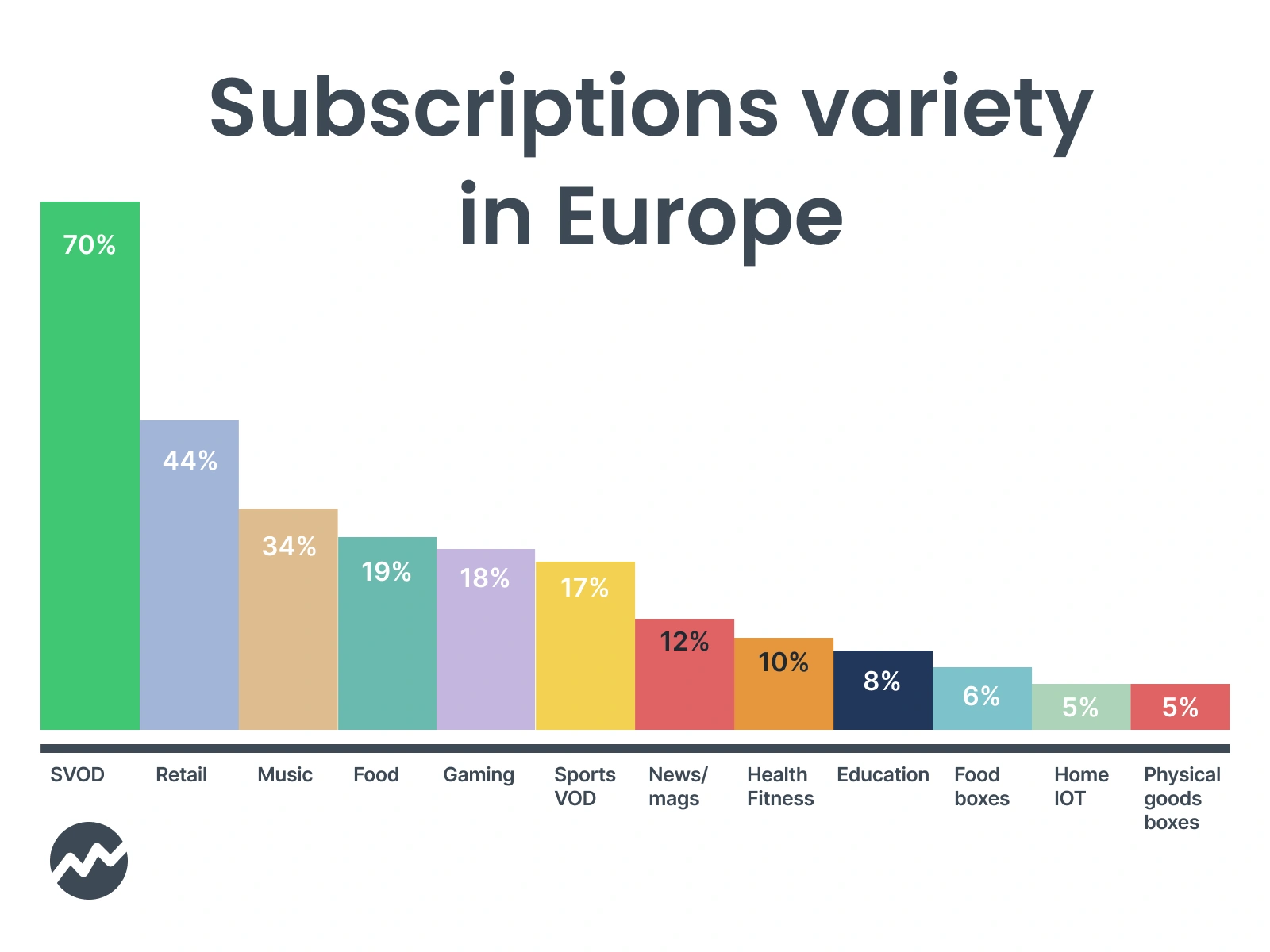

Did you know? A of 5,000 European subscribers found the average person had 3.2 subscriptions and spends €696 per year on subscription apps and services in 2024. In 2026, the number is even higher.

The demand for a single place to manage these payments is equally clear: 73% of consumers say they want one hub for all their recurring payments. Yet only 53% currently track their subscription spend at all - meaning roughly half of all subscription customers are going in blind every month.

That’s why subscriptions are one of the strongest forces guiding customer lifetime value in digital banking: retention, engagement, and transaction volume, all bundled into one recurring loop.

Subscriptions are no longer Netflix and Spotify

Subscription management used to be simple. You paid monthly for entertainment, maybe a gym membership, and that was the end of it. Now it’s everything.

Streaming, yes, but also software tools, cloud storage, delivery memberships, insurance, utilities, even certain healthcare services. Then come the payments that behave like subscriptions even when they’re not labelled that way: loan repayments, recurring transfers, automatic savings, rent, and “membership-style” services that bill you on schedule.

Did you know? Nearly half of consumers ( 47% ) say monthly subscriptions give them access to products, services, or a lifestyle they wouldn’t otherwise have.

Recurring payments are one of the strongest loyalty mechanics in modern banking. They happen automatically. They happen often. And they carry three things banks love:

- retention signals (people don’t change accounts when everything is wired up)

- revenue continuity (interchange and engagement don’t need to be “re-won” every month)

- data richness (recurring patterns are insight engines)

There is also a financial cost when banks fail to manage this well. Around 7% of all card transactions are declined industrywide, with insufficient balance being the primary cause. Declined payments cost banks the same as approved ones, generate zero interchange revenue, and can trigger scheme penalties at high rates. Subscription visibility - knowing what is coming before it arrives - is one of the most direct levers banks have to prevent that.

But none of that matters if your banking app can’t answer the most basic question:

“What is this recurring payment, and should I be worried about it?”

The three subscription strategies banks use

Most banks fall into one of three patterns. Sometimes they do all three, but usually one dominates.

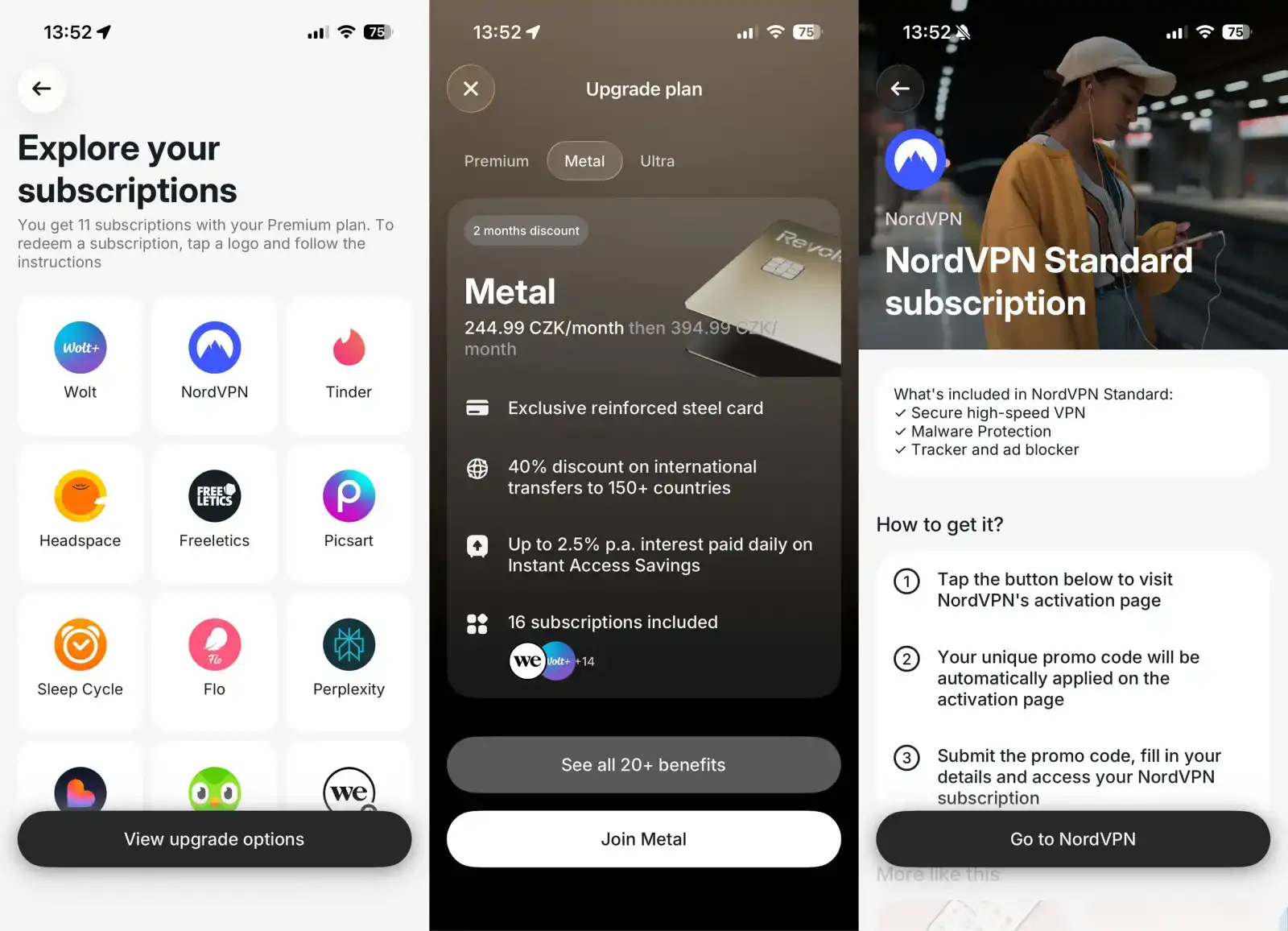

1) Subscriptions as perks

This is the bundle play: customers upgrade and get benefits like premium services, memberships, partner discounts, or lifestyle add-ons. Revolut is one of the clearest examples of this approach done intentionally. Instead of selling premium banking, Revolut positions paid plans as lifestyle bundles that include partner subscriptions like Financial Times Premium Digital, WeWork credits, MasterClass, plus other bundled benefits depending on the market.

It’s a valid model, but it’s where banks waste money fastest, because bundling the wrong perks is just paying for decoration. Customers don’t upgrade for generic benefits. They upgrade when the perks feel personally relevant – active users get a gym membership, movie lovers a Netflix subscription. Â

That’s where upsells work best, when they’re attached to a real moment of friction. The simplest example is ATM withdrawals. Revolut makes the “why upgrade" message clear by tying higher-tier plans to higher fee-free cash withdrawal limits. On Standard, users get 4,500 Kč (or 5 withdrawals) per month, while Ultra gets you all the way up to 55,000 Kč. Simple.

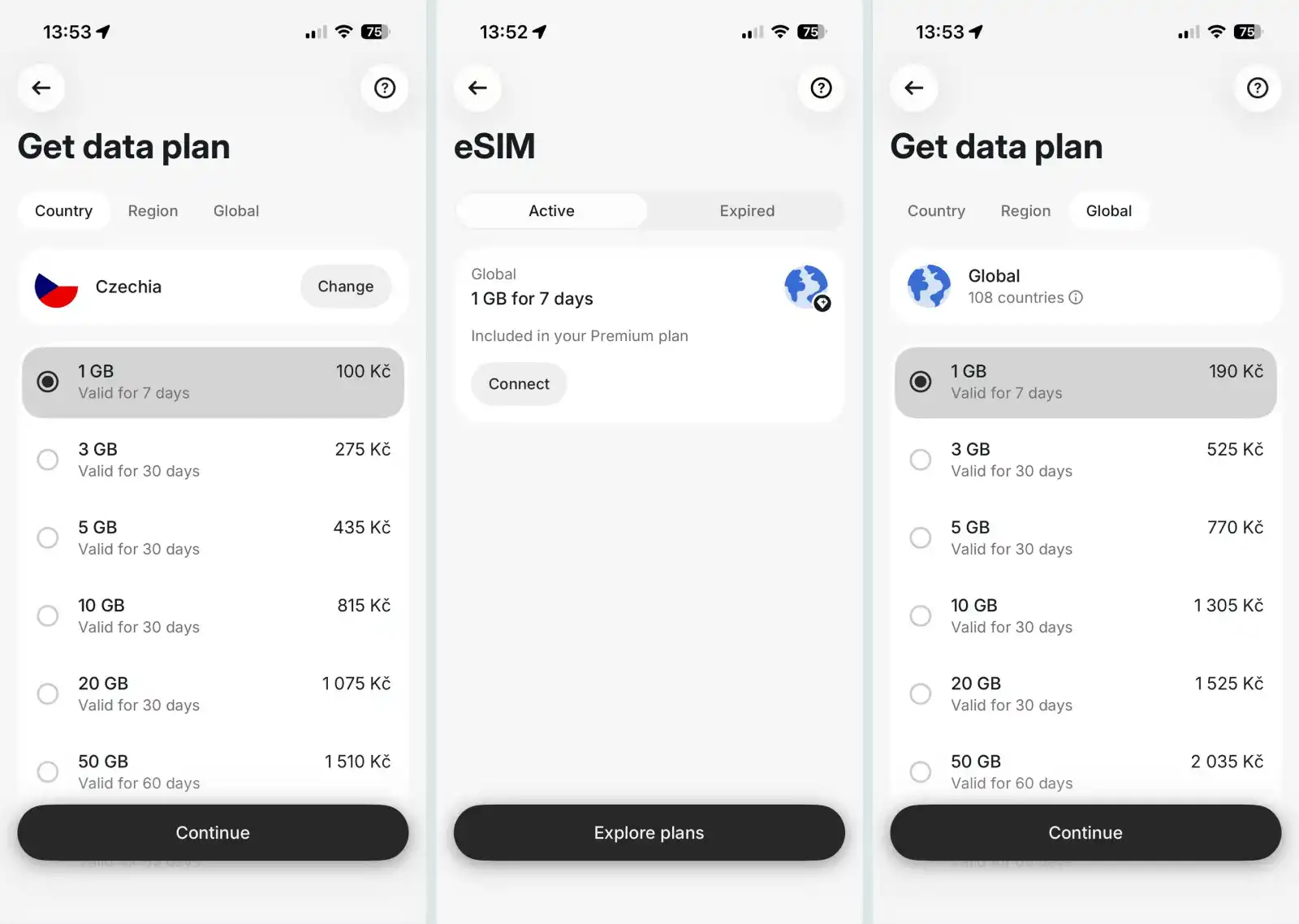

2) Features beyond banking

This is where the bank sells plans and tiers, but the real upgrade isn’t better banking. It’s bonuses and services outside of banking that make the account feel like a membership: travel connectivity, lifestyle access, protection, convenience, and fewer annoying surprises.

The cleanest real-life examples are banks and fintechs pushing into telecom, because mobile data is a universal pain point and it fits naturally into a bank app, especially for travel-heavy customers. Klarna Mobile offers an unlimited 5G plan for $40/month, fully managed inside the Klarna app. Revolut eSIM is built into the Revolut app as a travel-ready add-on, with 3GB per month included in Ultra and coverage in 100+ countries. Â

This is what “bank-as-a-subscription" looks like when it’s executed properly: the paid plan becomes a bundle of real-world utilities, and a customer doesn’t feel like they’re paying for premium banking.

The upsell timing still decides whether this works or fails. If you push premium before the customer experiences a clear “this app helped me” moment, it feels like advertising. If you surface the upgrade right when friction appears (roaming costs, travel prep, recurring spend pressure), it reads as a solution.

3) Subscription intelligence as customer value

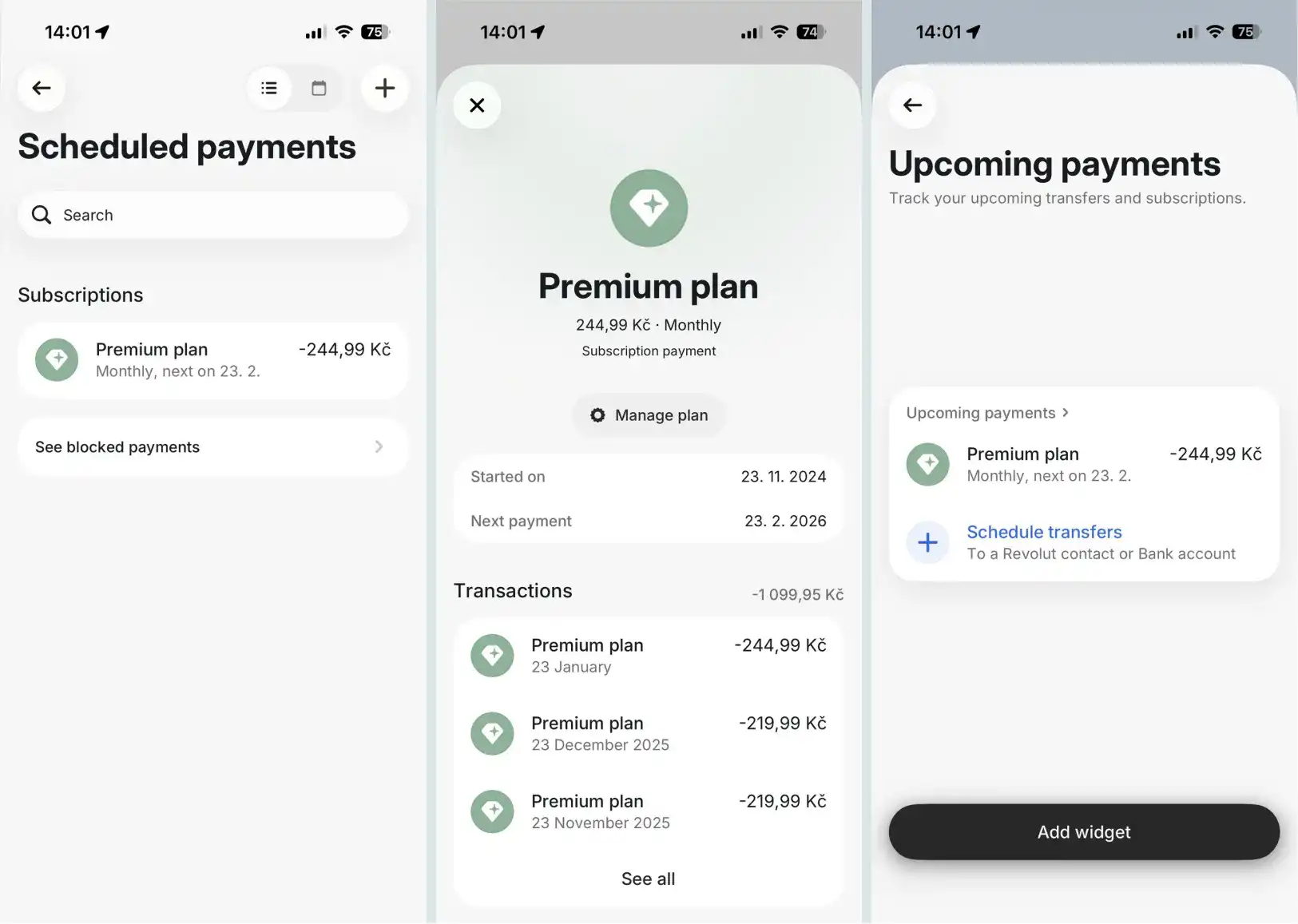

This is the most universal and most impactful strategy: identify recurring payments accurately, label them correctly, and give customers control. Revolut wins here again with “Subscriptions” feature, which pulls subscriptions, Direct Debits, and recurring payments into one place, then lets users track recurring payments, get notified before payments go out, and block unwanted subscriptions directly in-app.

It’s the approach that improves retention even if the bank never sells a premium plan. Because the app becomes genuinely useful.

This is precisely how recurring payments create primary-bank behaviour. Customers who can see all their upcoming payments in one place keep higher balances to ensure those payments clear. They open the app more often. They route their card-on-file credentials through the bank that gives them the clearest picture. Higher daily engagement, higher balance buffers, and top-of-wallet status - all driven by something as simple as showing people what’s coming.

And usefulness is the only loyalty program that works long-term.

Subscriptions are not only card payments

For years, subscription logic was basically: “if it’s monthly and paid by card, it’s probably a subscription.” That assumption worked back when most subscriptions were e-commerce. Now it’s breaking, especially in Europe, because subscription-like behavior increasingly happens through:

- bank transfers

- direct debits

- A2A payments

- mixed methods depending on merchant strategy

So, here’s the real issue: customers still experience those payments as subscriptions, but many banks don’t recognise them as such. They stay unlabeled, buried in the feed like generic transfers. And when recurring payments aren’t clear, the customer loses the one thing they expect from a modern banking app: a sense of control over what repeats.

A ĚÇĐÄlogo deployment in the Czech market illustrates this clearly. On top of 400 already-known subscription merchants, an additional 200 were identified through behavioural pattern detection alone. Among these were companies like Wolt, Foodora, and Rohlik.cz - all now ranked among the top 40 subscription merchants by volume. None of these would have been captured by a merchant-category approach, because their recurring payments represent a small share of total transaction count (just 1–5%), yet they account for a disproportionately high share of spending.

That’s why subscription management is ultimately a data problem before it’s a UX problem. Banks need the right enrichment layer to identify recurring patterns across rails, normalise merchants, and turn “random payments” into structured subscription objects that customers can understand instantly.

For more details on how enrichment solutions can benefit your bank, explore the ĚÇĐÄlogo offerings and our Recurring payments intelligence.